One of my favourite stories from the US election result last week was that of Théo. A mystery trader who “yolo’d $30m” on a Trump victory to return a reported “$49m profit in a week”.

What Théo had spotted, the story goes, is that if the polling question was: “Who are your neighbours voting for?” rather than: “Who are you voting for?”, Trump’s support went up several percentage points. So he commissioned his own poll, took a view, and put his money where his mouth is. Chapeau!

Théo here is displaying a “variant perception” – a posh way of saying he evaluated a market debate in a different way to most others.

Inevitably, almost all the speculation over the past few days on the likely impact of Trump’s victory does not display a variant perception. It falls into a category I would define as linear, fundamental analysis.

For example, Trump will put tariffs in place, so EU spirits are a sell. Or America First means a strong dollar, so EU imports decrease and rates stay low – and EU banks are a sell. Both are legitimate conclusions aligned with our portfolio.

What is the variant perception on the US election result?

As a natural contrarian, the majority of my most successful trades have come through taking a differentiated view from the market.

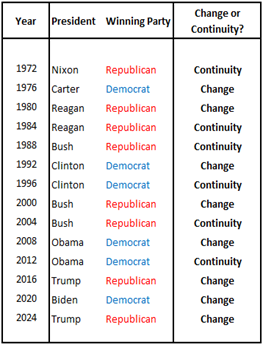

One way of thinking about an election result is to consider whether it represents change or continuity. The simplest way to determine this in the two-term-limited US is by looking at the winning party.

The results are as follows:

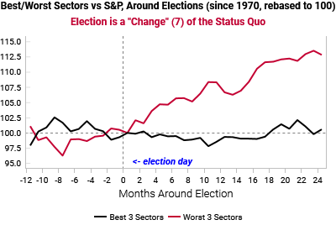

What impact does this have on the market? Interestingly – for the contrarian who tends to own things that haven’t done well rather than things that have – a political change normally leads to a market leadership change.[1]

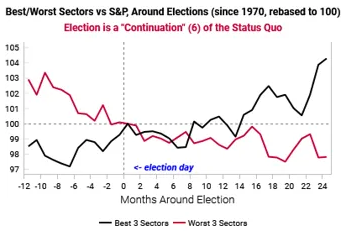

Could the change just be a function of four- or eight-year business cycles? Well, no – because after a continuity result, market leadership tends to remain the same.[2]

Elections that result in a change in governing party lead to a change in the best performing sectors in investment markets. Elections where the same party remains in power lead to a continuation in investment market leadership.

Let’s bring this analysis to the result last week. It’s (very!) early days, but so far the market has stayed true to form. And I do think the way the market behaves in the days following a US election are very informative, because they tell you a lot about positioning. Previously underperforming stocks seem to have caught a bid.

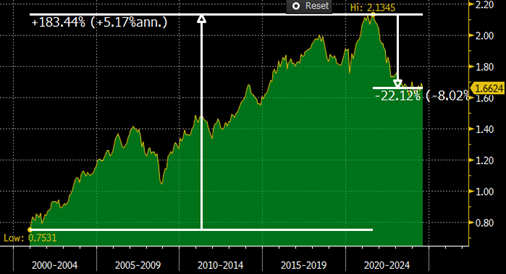

Readers will remember the Trump trade from 2016, when formerly unloved sectors such as banks and commodities performed very well initially. They then kicked on to become the so-called pain trade for the next 18 months as, one by one, clients capitulated and were forced to buy these stocks. “Panic early” was the best advice at the time. The same applied in 2008.

The equivalent pain trade for 2024 is almost certainly an underperformance of the previously “winning” large-cap growth, and the commensurate outperformance of small-cap cyclicality. Early market response in the US suggests this is in the offing.

Source: Bloomberg. White line is Russell 2000 small cap index, blue line is S&P 500.

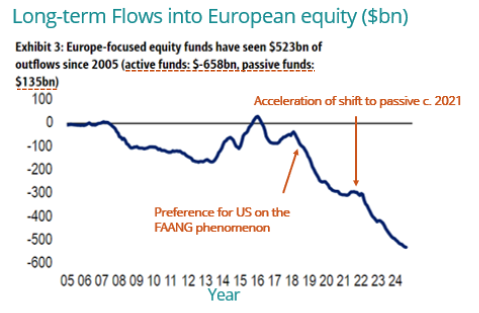

The reason this is so important is that the underperformance of small-cap stocks has been so profound that it has actually encouraged a shift to passive funds – which are typically much more highly weighted in larger stocks than their active peers.[3] It has been a huge drag on the entire active industry and has led to some anomalous valuations and investment opportunities.

Our fund currently has its highest ever overweight to small caps, on the basis that the relative outlook has almost never been so attractive. Most investors we speak to agree with the thrust of this positioning, but many struggle to see what will change the momentum.

If our read is correct, then, this election result – like the ones in 2008 and 2016 – could be the catalyst for a shift in the dynamic of market leadership.

Now is the time to put on our variant caps and wear our contrarian badges with pride.

[1] Source: variantperception.com

[2] Source: variantperception.com

[3] Source: River Global investors, Bloomberg, BofA.